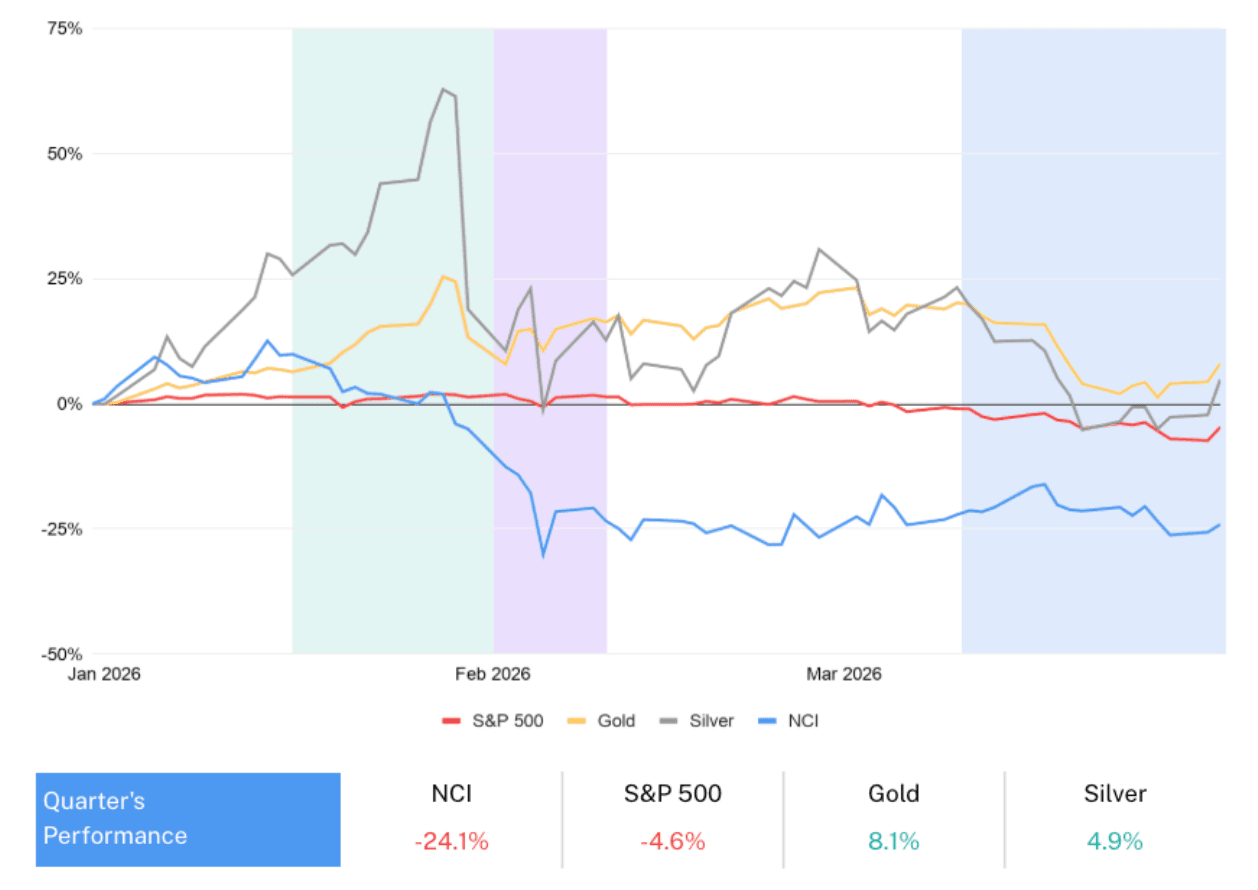

The first quarter of 2026 proved challenging for crypto. The Nasdaq CME CryptoTM Index finished the first quarter down 24.1% and at its lowest point, the drawdown approached 45%.

But looking back at Q1 with clear eyes, three things stand out to me that help inform where this market is going in the coming months—lessons about what this asset class is, how it behaves, and why the long-term case remains intact.

What happened? The Q1 selloff in three acts

The most important thing to understand about Q1 is that the drawdown had identifiable, explainable causes, and none of them were structural failures of crypto itself. As we describe in our Q1 Market Pulse, released today, the quarter unfolded in three distinct acts. The first act was the escalating US-Iran tensions in mid-January which triggered a classic risk-off rotation. Crypto sold off as a risk asset—exactly as it should in that environment—while gold and silver played their traditional safe-haven role.

Act two was Kevin Warsh’s nomination as Fed Chair catching markets off guard. Warsh has a hawkish reputation and his emergence as the leading candidate to replace Chair Powell effectively dismantled the monetary easing thesis that had quietly been supporting a range of liquidity-sensitive assets: crypto, gold, and silver alike. The probability of his nomination went from 29% to 97% in less than a week, meaning that markets had no time to adjust gradually. What followed was a forced unwind of crowded, leveraged positions. In that compressed window, crypto fell more than 31%, amplified by over $11 billion in liquidations.

Act three was the quarter's most counterintuitive episode. When the US campaign against Iran started on February 28, the traditional hedges (i.e., gold and silver) fell sharply. Crypto, by contrast, held its ground and recovered. The reason: precious metals had accumulated their own leverage through the prior period and were fragile heading into the shock. Crypto, having already been through its own deleveraging, entered the conflict with cleaner positioning and more resilient structure.

Geopolitical stress and monetary policy uncertainty shaped performance

Past performance does not guarantee future results. It is not possible to invest in an index and funds have other costs that impact final performance. Elaborated by Hashdex Asset Management with data from Bloomberg.

By March, the Crypto Fear & Greed Index had fallen to readings as low as 8 (on a scale of 100). The last time it was that low was after the Terra-Luna collapse in mid-2022, when a major protocol had imploded, contagion was spreading through the industry, and the broader macro environment was deteriorating with inflation running hot and rates rising fast.

Today's context is categorically different. There are no protocol failures, no massive fraud scandals, no systemic liquidity crises—but the fear readings are similar. That gap between sentiment and what the data actually shows is not a reason for concern. It is precisely the kind of dislocation that creates asymmetric opportunity for investors with a long-term horizon.

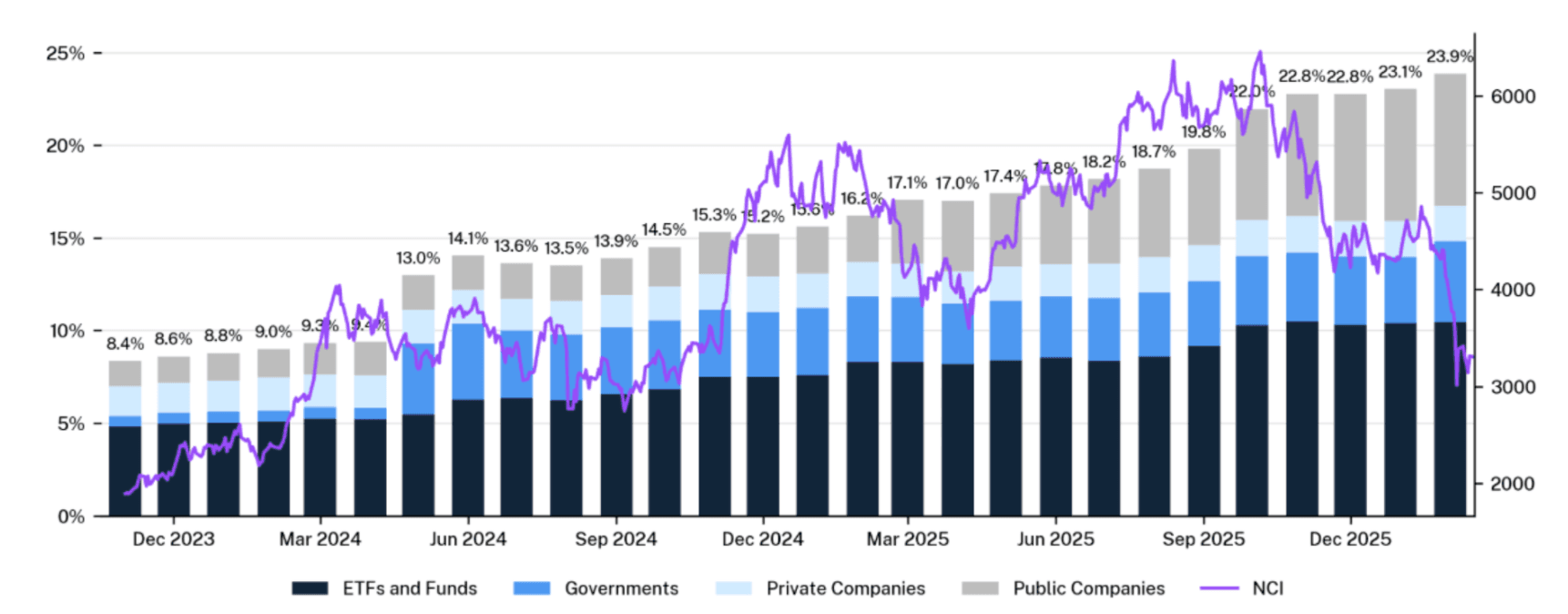

The most telling evidence is what was happening beneath the price surface during the same period of peak fear. Institutional holders nearly tripled their share of Bitcoin's long-term supply in two years, from 8.4% in December 2023 to 23.9% by December 2025. That accumulation didn't pause during Q1's volatility. As retail investors reduced exposure, ETFs, sovereign entities, corporations, and other institutional allocators absorbed the supply. The investor base is being rebuilt from the ground up, and the buyers stepping in at lower prices are precisely those with the frameworks, mandates, and time horizons to stay.

Institutions have nearly tripled their share of Bitcoin’s long-term supply since ETF approvals in 2024

Percentage of the LTH is calculated by dividing the whole LTH supply by the 5-month lagged institutional supply minus the outflow that happened in this period. Elaborated by Hashdex Asset Management with data from Bitcoin Treasuries and Bitcoin Magazine (from July 31, 2023 to March 31, 2026).

Our long-term valuation model captures this dynamic quantitatively. At quarter-end, crypto's market cap had fallen below the lower band of the model—a more extreme reading than either of the two prior instances that approached it. Those prior instances, in November 2022 and June 2023, were followed by 12-month returns of 318% and 177%, respectively. While past performance offers no guarantees, and this is not a call on timing, the pattern matters: historically, the zones of maximum fear in crypto, absent a structural crisis, have been the zones of opportunity. Q1 created that zone again.

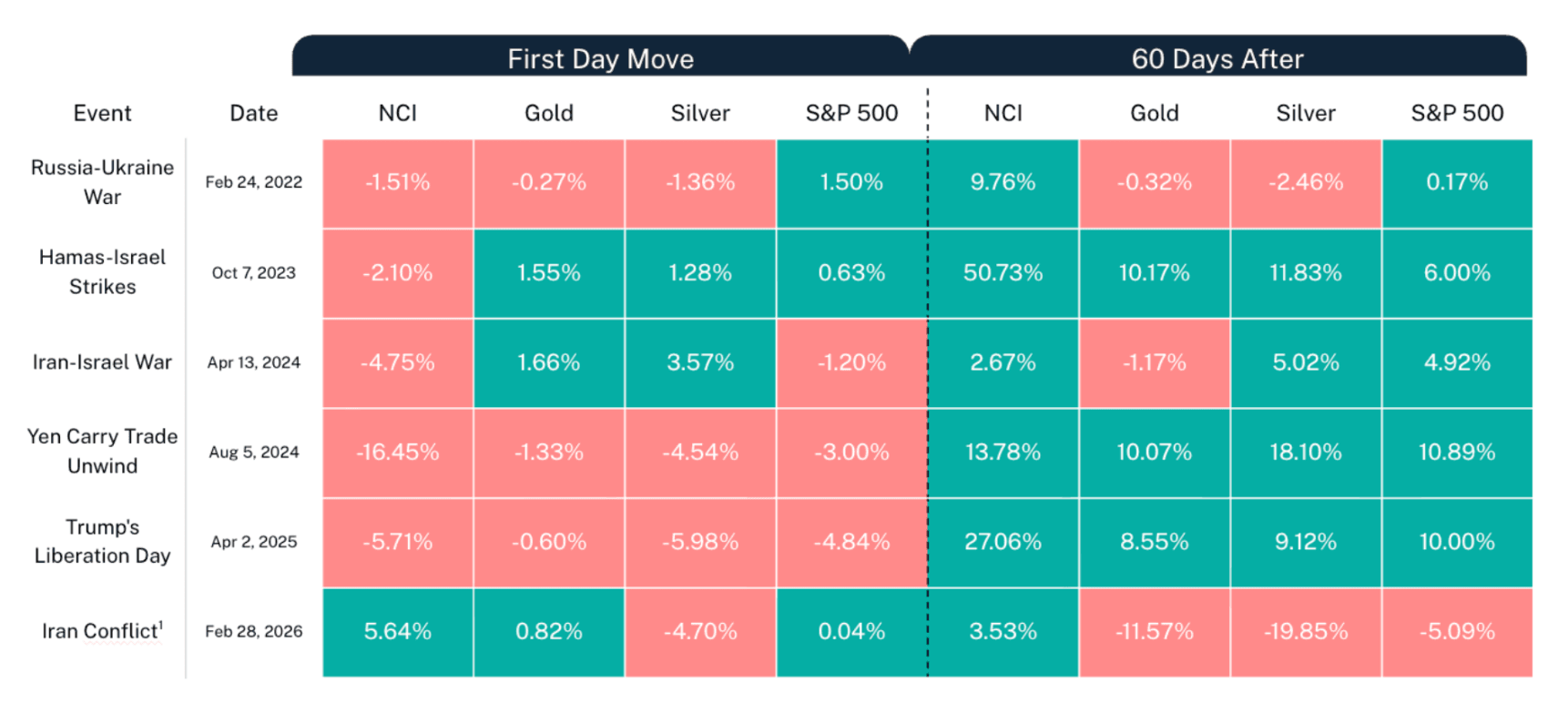

Across major geopolitical events since 2022, disciplined investors have been rewarded

Past performance does not guarantee future results. It is not possible to invest in an index, and funds have other costs that impact the final performance. Elaborated with data from CF Benchmarks and Bloomberg (from December 31, 2025 to March 31, 2026). [1] The 60 Days after performance is calculated from February 28, 2026 until March 31, 2026.

A strengthening foundation

Here is what I find most important about Q1: the price action and the structural picture moved in opposite directions. Prices fell sharply even as the regulatory and institutional foundation of crypto strengthened materially. That divergence is not noise, it’s the investment case strengthening in real time, while most investors were focused on the wrong signal.

The regulatory milestones of the past twelve months represent a genuine shift in the legal architecture of this asset class. The GENIUS Act signed into law, creating a framework in the US for stablecoins, and in-kind creations and redemptions were approved for crypto ETFs. And just last month, the SEC and CFTC issued joint guidance establishing the first comprehensive taxonomy for digital assets in the US, moving the regulatory posture from enforcement by ambiguity to classification by definition. Most crypto assets are now formally recognized as non-securities. The legal gray zone that has long been the primary barrier to institutional participation at scale is being systematically dismantled.

Additionally, the CLARITY Act—digital asset market structure legislation that Congress is currently considering—would provide the kind of legislative permanence that executive branch actions cannot. That permanence is what will help large allocators build full institutional infrastructure around crypto: custody frameworks, compliance programs, board-level mandates.

Why does regulatory clarity translate so directly into investment case strength? In the two years following bitcoin ETF approvals, cumulative flows into US crypto ETFs surpassed $70 billion. New investor types entered and institutional adoption accelerated. The rest of the asset class—including smart contract platforms, decentralized infrastructure, and tokenized finance—is earlier in that journey, with more potential institutional capital yet to enter.

Looking ahead: Q2 and beyond

There is a version of Q1 that reads as a warning: crypto fell nearly 25% in a quarter when equities barely moved, sentiment collapsed to crisis-era lows, and the asset class seemed to behave in ways that defied its own narratives. I understand why some investors read it that way.

But there is another reading I think is more accurate and more actionable: Q1 systematically cleared the conditions that had made the market fragile and brought valuations to levels that historically precede strong forward returns.

At the same time, the fundamentals kept moving in the right direction. Institutional accumulation continued and the regulatory framework advanced more in twelve months than in the prior four years combined. The investor base is growing more sophisticated and more durable.

Stress events in crypto have historically looked like failures in the moment and like entry points in hindsight. Q1 had real causes and a real impact. It also left the investment case structurally stronger than it was at the start of the year. That is the signal worth holding onto.

______________________

Effective January 20, 2026, the index changed its name from Nasdaq CryptoTM Index (NCI) to Nasdaq CME CryptoTM Index.

This material expresses Hashdex Asset Management Ltd. and its subsidiaries and affiliates (“Hashdex”)'s opinion for informational purposes only and does not consider the investment objectives, financial situation or individual needs of one or a particular group of investors. We recommend consulting specialized professionals for investment decisions. Investors are advised to carefully read the prospectus or regulations before investing their funds.

The information and conclusions contained in this material may be changed at any time, without prior notice. Nothing contained herein constitutes an offer, solicitation or recommendation regarding any investment management product or service. This information is not directed at or intended for distribution to or use by any person or entity located in any jurisdiction where such distribution, publication, availability or use would be contrary to applicable law or regulation or which would subject Hashdex to any registration or licensing requirements within such jurisdiction.

These opinions are derived from internal studies and do not have access to any confidential information. Please note that future events may not unfold as anticipated by our team’s research and analysis. No part of this material may be (i) copied, photocopied or duplicated in any form by any means or (ii) redistributed without the prior written consent of Hashdex.

By receiving or reviewing this material, you agree that this material is confidential intellectual property of Hashdex and that you will not directly or indirectly copy, modify, recast, publish or redistribute this material and the information therein, in whole or in part, or otherwise make any commercial use of this material without Hashdex’s prior written consent.

Investment in any investment vehicle and crypto assets is highly speculative and is not intended as a complete investment program. It is designed only for sophisticated persons who can bear the economic risk of the loss of their entire investment and who have limited need for liquidity in their investment. There can be no assurance that the investment vehicles will achieve its investment objective or return any capital. No guarantee or representation is made that Hashdex’s investment strategy, including, without limitation, its business and investment objectives, diversification strategies or risk monitoring goals, will be successful, and investment results may vary substantially over time.

Nothing herein is intended to imply that the Hashdex s investment methodology or that investing any of the protocols or tokens listed in the Information may be considered “conservative,” “safe,” “risk free,” or “risk averse.” These opinions are derived from internal studies and do not have access to any confidential information. Please note that future events may not unfold as anticipated by our team’s research and analysis.

Certain information contained herein (including financial information) has been obtained from published and unpublished sources. Such information has not been independently verified by Hashdex, and Hashdex does not assume responsibility for the accuracy of such information. Hashdex does not provide tax, accounting or legal advice. Certain information contained herein constitutes for ward-looking statements, which can be identified by the use of terms such as “may,” “ will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue” “believe” (or the negatives thereof ) or other variations thereof. Due to various risks and uncertainties, including those discussed above, actual events or results, the ultimate business or activities of Hashdex and its investment vehicles or the actual performance of Hashdex, its investment vehicles, or digital tokens may differ materially from those reflected or contemplated in such forward-looking statements.

As a result, investors should not rely on such forward- looking statements in making their investment decisions. None of the information contained herein has been filed with the U.S. Securities and Exchange Commission or any other governmental or self-regulatory authority. No governmental authority has opined on the merits of Hashdex’s investment vehicles or the adequacy of the information contained herein.

Nasdaq® is a registered trademark of Nasdaq, Inc. The information contained above is provided for informational and educational purposes only, and nothing contained herein should be construed as investment advice, either on behalf of a particular digital asset or an overall investment strategy. Neither Nasdaq, Inc. nor any of its affiliates makes any recommendation to buy or sell any digital asset or any representation about the financial condition of a digital asset. Statements regarding Nasdaq proprietary indexes are not guarantees of future performance. Actual results may differ materially from those expressed or implied. Past performance is not indicative of future results. Investors should undertake their own due diligence and carefully evaluate assets before investing. ADVICE FROM A FINANCIAL PROFESSIONAL IS STRONGLY ADVISED.